Stock Talk - DreamFolks: Riding the air travel phenomenon

DFS allows one to play the increasing air traffic trends, however the ability to scale up business is something that the company doesn't controls as it can't influence either demand or supply.

Elevator Pitch – “Company is run by first time entrepreneurs who had operational experience in the domain before starting the company. The company is a play on the increasing air-travel, enabling air-travelers to avail lounge services along with other loyalty solutions. The business is a network/toll-road operator with limited competition; however there is a large negotiating power among the banks which partners with DFS to provide these lounge services. The company has established a very strong hold on the Indian airport lounge operator business with ~68% traffic share and the company is diversifying its operations by expanding internationally as well as trying to add newer revenue streams from railway lounge and golf aggregation services.”

Divyansh’s Substack is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

DreamFolks is a 10 years old company (revenue XX Cr.) which is a service provider which acts as an intermediary between three entities:

The air travellers who are looking to avail lounge services

The companies which provide the lounge services

The credit card companies who are providing the customers the offerings of availing lounge services

To understand the business in a simple manner, one can consider DFS to be the VISA/MasterCard which is connecting the three entities and is operating the toll business enabling air-travelers to avail these services.

What are the product and solutions provided by DFS:

To keep it simple, DFS is connecting the users of credit cards to avail the loyalty solutions (pre-dominantly lounge services 95% of revenues) by forming partnerships with the

credit card issuers - who sell free lounge access, airport services such as meet and greet, baggage check-in etc., golf services as their differentiator for cards

lounge operators - to enable foot falls and providing POS terminal systems to do the authentication of the cards (to check if the customer has valid free visits, or not)

card users - to seamlessly avail these services by operating in the background.

The place where the solutions of DFS differs from VISA/Master is that DFS is providing an add-on to the customers by enabling a very niche use-case (airport services / loyalty solutions) rather than the wide use cases of payments serviced by VISA, Master.

Clients of DFS:

Credit Card Networks and Banks - The company has tied up with all the leading card networks (VISA, Master, Rupay) as well as forming direct partnerships with the banks (enabling them to customize the card reward offerings and probably saving on the cut that the networks would have earning). Among the Banks it has direct partnerships with HDFC, SBI, ICICI (i.e. the leading issuers of credit cards).

Lounge Operators - The company has inked agreements with all the lounge operators covering 100% of the lounges (54 in total) and with a few of the lounge operators it has also inked exclusive agreements.

Corporates (includes airlines as well as other corporates):

Airlines: While an airlines like AirIndia can afford to have its own lounges, other airlines (both full service as well as low cost carriers) dont have a lounge of their own. However their passengers might still want to avail lounge services or for specific set of customers the airline might want to provide these services (think Gold/Platinum Vistara tier), so these airline then tie-up with DFS to allow their passengers to avail lounge services.

Other Corporates: These may include online travel aggregators (e.g. Easymytrip which sells lounge services as a add-on during flight booking) or corporates which want to provide these services for employees (use-case is weak, however it is happening on ground)

With increasing income, people running short on time and desire to upgrade etc. etc. there has been an increase in the number of Indians who are travelling via flights. Given we all can relate to this phenomenon, there isn’t much data to be provided to prove this tailwind. Below are two charts which shows the increasing domestic and international air travel that happened in India over the last 6-7 years.

From a penetration/frequency of air travel perspective (refer image below), it appears that India is a very under-penetrated air-passenger market and has a decent if not a huge runway.

Privatization of airports: The Indian government has been slowly privatizing airports (Link) which is expected to bring operational efficiencies on the ground operations, what it also means is that given the travelling experience would become better and faster, there would be more people who would prefer to travel via airlines vs railways or other modes.

Opening of new/dormant airports: Given the multiplier effect that air travel has on the economy, and the general impetus by the govt. for creation of infrastructure, the number of active airports have jumped from 74 in 2014 to 148 by 2022 and plans are afoot for opening of 50 more airports (Link)

UDAN scheme: Since its launch in 2016, the UDAN scheme (Link) has connected/created new airport routes across the country and therefore enabled more air travel. While the flights might be limited, it also implies that the passengers who are taking connected flights might have longer waiting periods at the airports which in-turn promote usage of lounge services during the waiting period.

Background of promoter:

The company was started by three entrepreneurs, among which the key person being Liberatha Kallat who is the CEO of the company. Ms. Kallat before starting DFS had worked in the hospitality and consumer industry with Indian Hotels & Novotel and Pepsi Co. She later joined Plaza lounge as their business head for three years. Post which she started DFS. Given she has the experience in the domain, it is safe to assume that she would have figured out the pain in the lounge aggregation space and started DFS in 2013. When DFS started Priority Pass (“PP”) was already in existence and DFS was able to take away the market share from PP implying that the promoter/management team is doing something correct which helps it differentiate from the established players.

What is interesting is that when the company went for the IPO, the offer was 100% OFS and the shareholding at the time of IPO was 33:33:34 all between the three founders of the business, implying that the business doesn’t requires too much capital and is both profitable as well as cash generating.

Acquisitions: In Mar’23 the company has acquired 60% stake in Vidsur Golf which is in the Golf aggregation space for 1.5 Cr. similar to DFS which enables customers to avail lounge services, Vidsur enables customers to avail golf training and playing sessions. Apart from this, there hasnt been any acquisition by the company.

Non-financial Performance:

The key metric to track for the business are:

Air traffic

Credit Card

Passengers availing lounge service

Below are the data points for the past 24 months

While the earlier periods of FY 22 was on a low base due to Delta wave of COVID-19, one can see the resurgence of air traffic at the airports as well as people using lounge service which has been on an uptrend both on absolute values as well as %age basis reflecting increasing tendencies of air-travelers to avail these services.

BUSINESS ATTRACTIVENESS

1) Strongly differentiated business model -> High

Network business which is tech enabled

Business growth is complemented by limited on-ground operations to form partnerships with both sides of the network i.e. issuers and lounge operators

2) Competitive Position getting stronger/weaker -> Can’t say

DFS already dominates the market with 68% market share the company is very strong in the Indian domestic air-travel eco-system, and therefore the company might already be at its peak with respect to competitive positioning

The company needs to build its strength in the international market, which would be more dominated by Priority Pass

3) Next Level of business -> Can’t say

The company is currently a one-trick pony (though a very strong pony with a long growth runway ahead for itself) and is trying to enhance its value-proposition by making acquisitions in the golf aggregation space

Demand/Supply levers: Being a network play, the company can’t influence the supply or demand of the services, that work needs to be done by the card issuers or the lounge operators; thus DFS has limited control over driving customers to avail its services.

International Expansion: The company has hired a head for international expansion, no updates have been shared by the mgmt, but has mentioned that it’s going to be 1-3 years kind of wait

4) Value Migration Curve -> Can’t say

The company is sort of dominating the lounge aggregation space and through its acquisition of Vidsur Golf is trying to enter into the Golf aggregation space; however beyond the aggregation space (lets say horse riding or some other things), right now its not clear what the company can perse do, as they dont own the customer, and are a hidden brand

5) Quality of earnings -> High/Medium

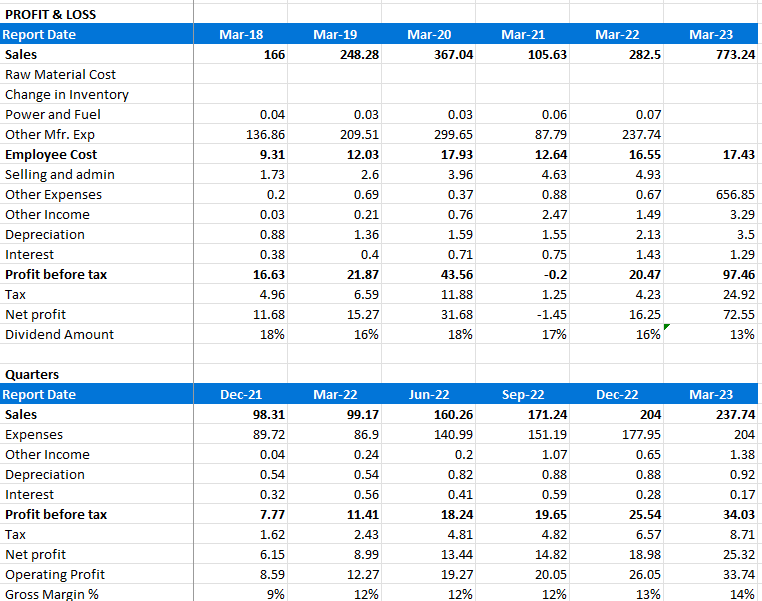

Sale is a bit lop-sided with Q1 being slow (less holidays and weather not being that conducive for travel), however the business ramps-up as we move towards Q4; however from the air passenger traffic trend its largely uniform with slightly higher traffic at the FY end

Air Traffic by quarters

Pricing power: For the time being the company has been able to maintain its gross margins at ~14-15%, however the company does faces a strong vendor base in the form of banks/card issuers who would always look at minimizing their costs, from some industry sources, it appears that the banks fund 1.5-4.5% of the gross margin, with the remaining 10.5-13.5% being funded by the lounge operators, and that is a relatively weaker side of the vendor eco-system for DFS.

Converting profits into cash: Medium

While the company has been reporting good profit growth in years of normal air traffic, the same is not converting into cash in a similar manner. The (CFO+Tax)/EBIDTA totaled over 5 years is running at 56% which is a middling number, neither here nor there. However one benefit of doubt needs to be given to the company that among the last 5 years, there have been COVID related complications as well as the company has grown with internal accruals and no VC funding, so reported profits do convert into cash albeit in a delayed manner.

6) Key growth drivers

Increasing air travel

Increasing card penetration (either credit card or debit cards)

International expansion: The company is expanding into the south east Asian market by setting up a subsidiary in Singapore and the management mentioned that their clients have asked them to go establish Singapore operations. However it is not clear, who is the target customer (Indians who are using lounge in Singapore which are being serviced by Priority Pass, or is it Singapore customers who travel a lot internationally)

7) Intellectual Property – Low

The company has its own in-house tech team which has developed an API based loyalty system on which DFS is running its operations; the system seems to be capable for scaling-up (as depicted by the company’s) ability to support increasing lounge users without any issues which might have come in the news. However to say that the company has something unique in its systems seems unlikely, as the system is running on standard POS rails and can be replicated by other POS players (say Pinelabs)

8) Profitability Drivers

Few things to note:

Look at the gross margins % stable operating in the range of 13-15% (the expenses in the quartely P&L includes all the costs including tech, people etc.)

Employee expenses being low double digits inspite of the revenue moving from 166 Cr to 770 Cr (the company had 60 employees at the time of the IPO which has increased to 70 since)

The profitability driver are just two simple metrics:

Air Traffic

Gross Margins negotiated by the company

KEY MONITORABLE

a) Capacity at the lounges: While the air traffic can increase at a higher rate (supported by more flights), the capacity at the lounges is limited by the real-estate that they are operating and given congestions at the airports as well as other stores, increasing the lounge areas is not an easy option. However the avg. area of lounge has been growing over the years, but there is a limit to the expansion.

Source: DFS DRHP

b) Competition: Currently the space is dominated by two players DFS (68% market share) followed by Priority Pass; While for PP India might not be the biggest of the markets to focus on (they are more dominant in the premium and international travel lounges), the space and margins seems to lucrative for some one to not enter and capture.

c) Free lounge visits: To be honest, if the lounges are made chargeable to customers, the traffic is bound to reduce dramatically, and therefore the number of free visits that are made available by the card issuers is an important driver for DFS’s revenues, however it is difficult to track, and ad-hoc articles might reflect card player activities in the area.

Summary:

DFS is a strong proxy for the increasing air travel and one can consider the company as a potential investment if they are looking to play the air traffic phenomenon, without taking sides on which airline is going to win

The gross margins are attractive at 15%, and can attract competitions (though globally there hasn’t been any large scale player who has entered)

The company enjoys a very high operating leverage, as the only expense after the gross margins are the employee costs which are growing very slowly, and thus any increase in traffic, flows directly to the PBT

The company is trying to expand its market both in geographic terms (Singapore expansion) as well as product offerings (railway lounges, golf aggregation), however the success of these are yet to be ascertained

Few challenges that the company might face:

Limited capacity at lounges slowing down accessing lounge services by customers

Margin pressure being exerted by banks

New entry by players who already tech/payment provide services to lounge operators

Sources referred:

1) Balance sheet and Financial schedules of the company for breakup of expenses

2) Management Discussion and Analysis, Transcripts and Investor Presentations

3) Annual Report and Investor Presentation, Transcripts and DRHP

Disclaimer: Not SEBI registered, views are personal and just capturing my understanding of the business. Invested in the stock as a tracking position, views may be biased

Divyansh’s Substack is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.