Stock Talk - Singer India: Worthwhile to explore?

Stock Talk - Singer India: Worthwhile to explore?

Quick Introduction of the company

Singer India (Link) is a brand name, that most of us can recall very easily; its the ubiquitous sewing machine company that our parents would have at-least bought once in our life and is among one of the most trusted brands in India.

: Amazon.in: Home & Kitchen")

Sewing Machine which is usually present in a middle-class family’s assets

Growth

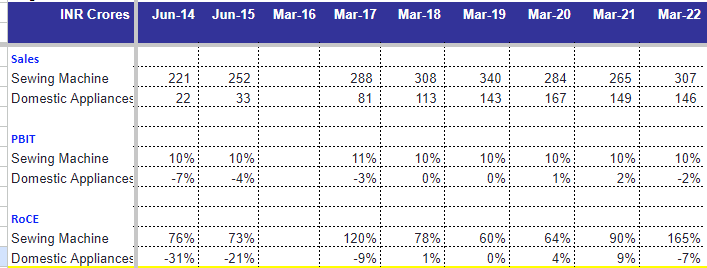

At an overall level, one may see that revenue growth over the last ten years have grown at ~10% which seems to be a good growth rate given that the sewing machine industry itself is growing at about 2-3%, which would imply that Singer has been taking over the market share from un-organized market.

However, if one looks deeper, and understand the composition of the revenues, one sees that the company has introduced a new category of products i.e. consumer durables, and its the consumer durables business which has been driving the revenue growth through launch of 24 categories (e.g. washing machines, ACs, fans etc.)

And therefore, it becomes clear that the company is losing out its market share to other players (namely Usha which is another big brand in the sewing machine industry), which is also mentioned by the company in its annual disclosures:

Segmental performance:

While the company has been growing its sales in the consumer durables business, its not necessarily flowing to the bottom-line, as the business itself is loss making (one can’t necessarily blame COVID as a reason for loss, as the growth of consumer durables actually increased during COVID as well as FY 22 was not affected by COVID)

However, the Sewing Machines business has been the consistent performer for the company with a high return on capital employed, and one can say that the company is utilizing the profit generated by the sewing business into developing new business category (which is a good thing), however it seems that in the consumer durables business the company hasn’t been able to find its niche.

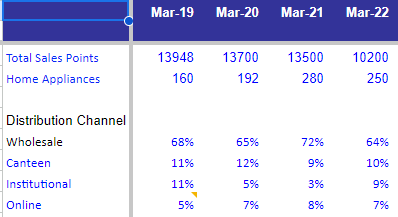

Volume Trends

The last four years of volume trends points to lower volume throughput vis-a-vis Mar’19 (last year not impacted by COVID) across both sewing machine as well as consumer durables. While lower throughput might not be necessarily bad if the mix is changing towards premium products, but that too isn’t happening.

Manufacturing and Distribution:

Manufacturing

The company had a manufacturing plant in Jammu, which was sold off in FY 23 (company disclosures) and no new information has been released on the new plant. Given the political situation in J&K and lower margins clearly point to the fact that the company is mostly into the trading business (Ludhiana is a big center for Sewing Machine manufacturing, Consumer Durables seems to be more imported business as reflected by higher and increasing imports holding at ~13% of sales)

Distribution

As the company is more in the trading business than manufacturing the extent of sales points/distributors that the company has becomes very critical in driving sales. However, if one looks at the last four years of performance, we see that the sales points are actually reducing, which doesn’t looks good for the company, esp. since wholesales distribution constitutes >60% of their sales.

Summary of the current business performance:

As one might have guessed, this company seems to be caught in a rut, not being able to scale up its core business neither able to scale up the new business. From the management commentary, the management seemed content and not showing enough aggression, and if one looks at the financial ratios, there isn’t a good picture either.

So why am I writing this post:

What’s changing:

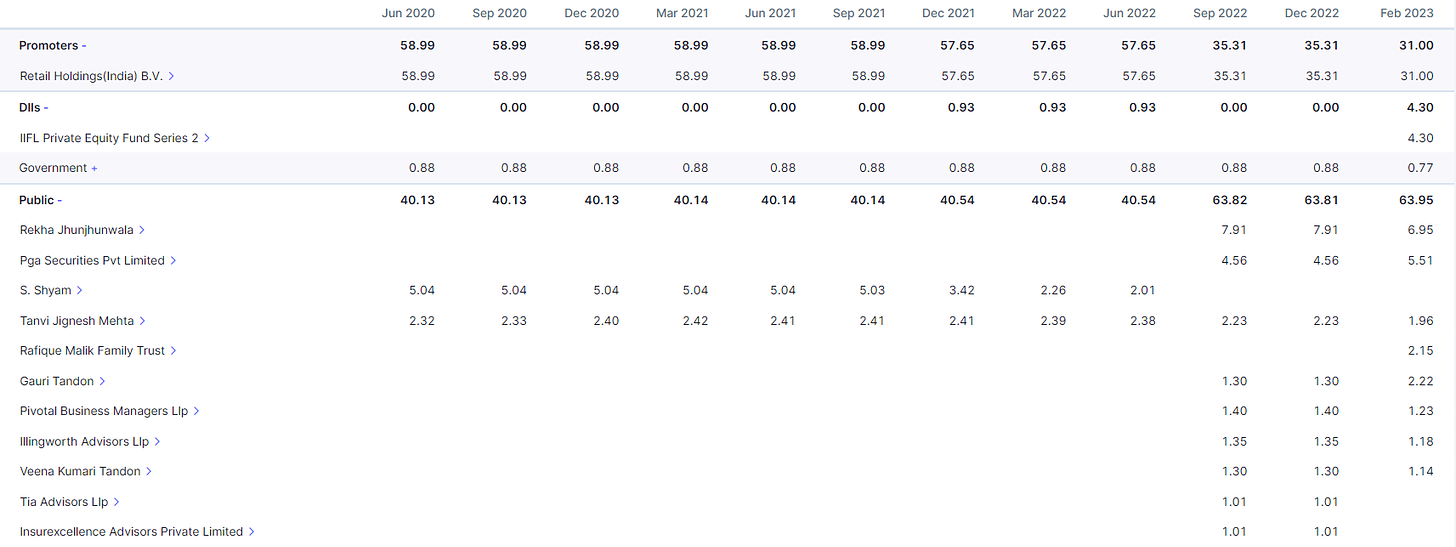

Shareholders:

Owner: On face value, one doesn’t sees that there is a new owner who has come-in, but what has happened is that the entity which owns Retail Holdings, sold its entire holdings to two PE investors

The PE investors based out of UK (actual names not disclosed) seemed to be experienced players in this domain of scaling/turning around sewing machine and consumer durables business (Link)

Addition of marquee name: The investment in Singer was the last investment of Rakesh Jhunjhunwala

Issuance of preference share: In Feb 2023, the company issued preference shares to IIFL to raise 56 Cr. coming into the company

Shareholding Pattern New management: Rakesh Khanna (who led Orient Electric till now) joined Singer India on April 6th (Link)

So there seems to be a lot going at Singer:

new management is focusing on driving new changes,

infusing energy into the brand Singer, getting new jockey (i.e. the CEO),

raising new funds for the company to fund growth

But the above isn’t missed on the market:

What should one do?

While the new promoters are striking the right notes, the turnaround of Singer is going to take a couple of years atleast, with the company:

Doing new product designs and launches

Either go the manufacturing route (seems unlikely) or increase the points of sales selling their products

Do enough marketing to increase its recall in the competitive consumer durables business.

My take is to just wait for an year, to figure out what is actually planned by the new management, before taking in the plunge.