MapMyIndia is over 25 years old company (revenue 260Cr) which is a product company specializing in providing mapping and IoT solutions across multiple industries. The company is based out of New Delhi and mostly services Indian customers. However the company earns revenues in foreign currency as well (~30%) which is Indian clients using their services in foreign markets. The company has developed all its solutions in-house, however post IPO the company has made certain acquisitions which as per management are either back-ward (enabling MMI to reduce costs e.g. Drones) or forward integrations (e.g. GTropy which is a devices play using MMI tech)

What are the product and solutions provided by MMI to clients:

Digital Maps

Navigation & Analytics

In-car vehicle navigation solutions

Vehicular telematics

ADAS, Autonomous driving

Land Surveys

Map development and integration services

Allows their map data to be integrated with third-party service providers to develop solutions for their end-customers

Location based Analytics / Geo-spatial Analytics

Market/location mapping wrt to demographics, demand, heat-distribution mapping

The business can be seen from two lenses:

End-user industry

Nature of service

End-user industry: The company services two kinds of clients a) Automotives & Mobility (46% FY 22 and 53% 9MFY23) b) Consumer Tech and Enterprise (54% FY22 and 47% 9MFY23 revenues)

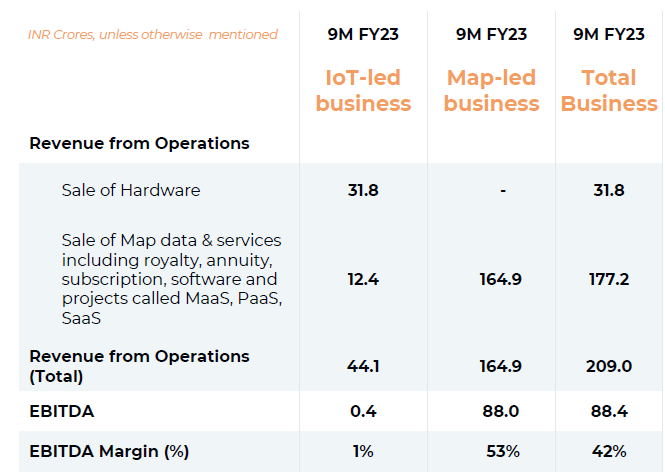

Nature of service: The products and services that the end-user industries avails from MMI are a) Map Data & Solutions (~78% of 9MFY23 revenues; ~34% FY22 revenues) and b) IoT solutions (~22% of 9M FY23 revenues; ~66% FY22 revenues)

Clients and Solutions provided by MMI

Automotives and Mobility (A&M) has been the earlier bread and butter business for the company, but the company started to diversify into other industries which are looking at location specific solutions (C&E). Their client list includes:

Automotive & Mobility: 4W: MG, Hyundai, Maruti, Mahindra, Volkswagen, Toyota?, Ola & Uber Cabs, Nisaan (some limited solution), 4W EV OEM, EV CV (battery solution), Kia, Avis Car Rental, Honda (basically Tata Motors [they use what3words which is UK based, maybe JLR connection], Renault are missing), Safexpress 2W: Bajaj Chetak, 2W OEM x 2 (Ola Scooters, Hero, TVS, Suzuki)

Revenue Model: Per-car per-year revenue model which is fixed and accrues over 3-5 years, additionally there are top-ups around additional APIs consumed by customer or new services introduced by MMI. Deal with OEM is model specific and the OEMs can cancel order or not continue without any penalties

Consumer Tech - Private: PhonePe, Yulu, Flipkart, Airtel, McDonalds, Bajaj Super App & Bajaj Finance (Super-App: Cust Geo location, merchant mapping; Enterprise: KYC & Fraud Analytics with location flavor), HDFC Bank, 2 Banks + Fintech, Cars24, Cement Company, FMCG x2, CRM SaaS, Social Media (FB?), Apple Maps; Grofers (now Zomato), Amazon Alexa, Clients acquired through their Gtropy acquisition: HMIS, Mahindra Logistics, Diageo, Suzuki (CV?), JK Cement, Wonder Cement

Solutions provided includes: Sales and Operations Planning by location, store launch planning, workforce monitoring, lending location analytics, Location Demographics, Security Solutions & Vehicle and Assets Tracking, EV charging station mapping and navigation, digital twin city mapping in 4D, distribution analytics, safety mapping for long-distance routes, consumer location insights for marketing. For telecom and utilities, it provides RF and optical fiber mapping, field force monitoring, line of sight analysis for 4G/5G planning

Revenue Model: Per-API consumption billing as well as come one-time customization & solutions development

Consumer Tech - GoI: Central, State, District government and Govt. Departments are clients looking at providing public infrastructure services to citizens

Solution provided includes: Crime mapping and analytics, Live Transport Tracking (Delhi, refer One Delhi app; UP Live Traffic monitoring), Company Location mapping (to identify Shell companies), Smart City solutions, Healthcare Infra mapping (used in COWIN portal), GSTN, CBDT, Umang App location based services, ULIP (Logistics portal)

Revenue Model: Direct contracting with Govt as well as part of bids won by systems integrators; while they haven’t mentioned, but revenue model might be mix of both fixed and API pay as per consumption model. Company wants to limit direct Govt revenue to <20%

Consumer Tech - B2C: Not a big focus area as of now (probably given Google’s dominance). However the company has launched Mappls product which provides Google Maps functionality and ++.

Solutions provided: Same as Google Maps, 360 degree view, street view etc

Revenue Model: On the pure navigation maps: Not yet figured out, the company doesn’t want to focus on ad-based monetization

Revenue Model: On the devices that MMI has started selling, its mix of device sales + subscription income accrued over years. For Rs. 100 of device sales, the subscription revenue is 33-40 Rs. However in the initial periods, the margin will be depressed due to device margin being lower, but later on the subscription revenues will start accruing at a higher margin

Summary of the solutions: MMI intends to add a location flavor to any of the analytic requirements of the clients and provide real-time feed to customers. While automotive is an obvious industry, MMI is expanding to other industries to provide mapping, workforce & asset optimization, geo-spatial analytics, and security solutions.

MMI’s solutions are all cloud/tech enabled with all the functions being serviced from two office locations, the business is tech and people heavy (like any tech service provider); the maps data needs to refreshed periodically and the company has developed in-house expertise to update these maps through remote-sensing, street view mapping as well as on-field person led updation of the data, which acts as a key differentiator for the company.

Liberalized the sector by removing requirement of approvals for surveying, preparing, storage and dissemination of geospatial data for Indian Owned or controlled company

Govt issued Geospatial guidelines, which barred foreign companies from:

vehicle based ground survey

street view survey

acquiring, reselling or reusing granular level mapping (1M horizontal and 3M vertical)

cannot reuse or resell the data and cannot store the data on their servers

IMPACT: Initial expectation was that Google might face challenges due to the above limitations, however they have formed a partnership with TechM [Indian] and Genesys [Indian] (Link) as a way around the regulations, so short-term impact might not be much for Google, long-term implication not sure.

AIS140:

ADAS (Advanced Driver Assistance System) to be rolled-out by 2022, while the timeline has slipped, there were announcements that the Govt wants to make ADAS compulsory across models. Might not have happened in 2022, but might happen say within 3 years? Smaller solutions might happen within this time-frame like collusion warning system, lane departure warning, automatic emergency brakes. Overall timeline 2030.

All state and institutional buses to have vehicle tracking, camera surveillance and SoS system

IMPACT: Large demand for A&M and IOT solutions, Delhi and UP have gone live with MMI. Given MMI’s relationship with GoI, they seem to be getting preference in getting GoI orders. Other states might go through a tender approach, but given actual solutions, barring of foreign companies, large chunk might be expected to come MMI’s way.

Drone Ruling:

Foreign companies barred from entering the market.

Drone based delivery within corridors to be facilitated by the Govt

IMPACT: Need for Geo-spatial solutions to go-up as drone use-case and requirements would go-up; the jump might be rapid rather than gradual.

CCI Google Ruling: CCI’s ruling on Google forcing them to open the Google Android ecosystem and unbundling/removal of default apps might open a B2C channel for MMI to form OEM partnerships. However realization of this might be a long shot.

GPS based Fastag:

Instead of the current Fastag solution, proposal has been made to introduce GPS based Fastag solutions with vehicles fitted with GPS devices being used for tolling services. Timeline not defined.

Customer Tailwinds:

Cyclical:

Automobiles are expected to have a good economic cycle for the next two-three years, and semiconductor issues seems to have been sorted out. MMI has more than 80-90% market share. Driven by regulations, vehicles are expected to be fitted by these GPS/Navigation solutions. Revenue from such contracts are expected to be realized over 3-5 years. Annual sales of 4W ~ 3Mn/year

Similar to 4W, 2W also expected to go-up in demand; given presence with Ola 2W, TVS, Hero, Suzuki. However in 2W the scope might be equally large, given the increasing penetration in 2W EV Sales, which includes high penetration of MMI’s solution. Annual sales of 2W ~16 Mn

Secular:

Consumer: More digitizations and start-ups looking to provide personalized experience, any business involving movements (either factor to warehouse, or warehouse to customer) is a potential use-case. However no numbers available/researched/estimated.

B2B: Digital transformation of companies, India push for manufacturing and the Industrial Revolution 4.0 i.e. IoT enabled manufacturing is a use-case for the company, however MMIs TAM is limited to analytics around market entry, continuous movement monitoring

Therefore MMI is present in industry which has regulatory tailwinds, which are supported by customer behavior of wanting things done digitally or involving technology to digitize their processes to being in more efficiency. While the company’s revenue are tilted/dependent on Auto which is a cyclical industry, the current upswing expected in mobility supports MMI’s growth. The industry seems to be a diffused one with multiple players operating in the domain, but as a brand name MMI has been able to achieve a customer recall.

Elevator Pitch – “Company is run by experienced technocrats and is a play on the digitization of supply chain/logistics theme, providing geo-spatial analytics and experiences to customers. As the business is dependent on the maps data generated over 25 years of operations, there is a very high operating leverage component that is supporting the company’s profitability. The company has established a very strong hold on the 4W navigation/telematics product offerings and is also making in-roads in 2W EV markets as well. In order to diversify their dependency from the automotives sector, the company is also developing relationships with other industries and developing solutions for them riding on their maps data.

Additionally, the company is trying to make a B2C play through the acquisitions that it has done GTropy which is focusing on selling IoT devices (mapplsgadgets.com) and then getting a subscription revenue over the period of time, in addition to this the company’s solutions are map data agnostic and therefore the company is trying to expand overseas targeting the APAC+US market”

Background of promoter and business theme:

Technocrat Promoters: The company was started by Rakesh Verma along with his wife in 1995 and started building digital maps for India. Over a period of time, the company kept introducing new products with MapMyIndia launching a pan-India navigation system in 2004 (this launch was done by their son Rohan Verma now CEO of MMI), and subsequently the company has been launching newer offerings from their side as well as upgrading their offerings. For a broad history of launches, refer below. The company has been expanding its product offerings through a mix of in-house tech developments and acquisitions.

Quality of Product:

1) Given automotive product cycles take multiple years, and difficult to change in between, MMI has been able to service the customer navigation requirements, won order, won new clients, and also up-sold their services to clients. For e.g. for an OEM chose to upgrade the offerings provided by MMI to also include ADAS solutions (maybe MG?)

2) Customer retention has been high across the three reported years by the company, depicting the reliability of the product and offerings

3) Operating at Scale: When the COWIN portal was first launched, there was a delay in response time, but the company scaled up the response time to offer services which was used at Pan-India level and also probably with high concurrency

4) Dominant market share: 80% market share in car navigation

5) MG motors shifted from TomTom to MMI (might be regulations, might be better India Maps data)

Management’s ability to think and execute strategically:

1) Building the business over 25 years, with focus on cash generation (limited capital dilution, promoter holding 53%)

2) Focussing on client wins as well as retention

3) Using acquisition as a strategic tool (refer below)

Acquisitions & Investments: The company has done multiple acquisition, and the pace of the acquisition have increased since the listing happened. As per the management, the acquisitions have been done with an eye on the use cases that exist for which MMI doesn’t have the know-how, or it would help in backward integration or lending the brand name of MMI to help scale up the acquisition.

Among the acquisition, for two the product have already been launched by the company:

Pupilmesh: This is a helmet which takes data from the MMIs maps data and provides turn-by-turn navigation to customers, which avoids the phone stand mount installed on the 2W which also forces the customer to keep looking at the phone for navigation

Gtropy: This is a multiple device solutions that the company is rolling out focusing on providing GPS and navigation solutions to vehicles which are already on road. While the company GTropy was earlier focusing on logistics use cases, under MMI they have introduced multiple other hardware products.

Trackers

Dash Camera

Navigation Dashboards

Example of the Pupilmesh solution: Augmented Reality solution for driver eye-level navigation guidance system

Example of the Gtropy solution: IoT Device and Solutions focusing on logistics space

BUSINESS ATTRACTIVENESS

1) Strongly differentiated business model -> High

a. Company is playing on its IP theme of map data aggregation and detailing

b. Market seems diffused with a multiple players existing, however not all players seems to have an integrated offerings

c. MMI claims to be only player having a full tech stack of locations analytics and the analytics solutions is map data agnostic

d. Strong grip on the 4W auto market and being able to both retain and up-sell solutions

2) Competitive Position getting stronger/weaker -> High

a. Regulatory tailwinds to limit entry of foreign competition, leaving a wide space for MMI to grow & capture market

b. Company is integrating the hardware and software solutions to provide a comprehensive/well integrated offering

c. However risk remains of international players partnering with IOCC to provide similar capable solutions

3) Next Level of business -> Can’t say

a. Should become the default/standard choice of govt contract where nomination works given long history of business, delivery of large scale govt projects

b. While the space seems to be very wide (anything to do with a location attribute), the use cases are hazy i.e. they exist but how much will be formalized and captured by MMI is not clear.

c. Multiple acquisitions, need to evaluate how they integrate and deliver. Gtropy and Pupilmesh have been scaled-up however other acquisitions needs to be seen

d. International Expansion: The company has hired a head for international expansion, no updates have been shared by the mgmt, but has mentioned that it’s going to be 1-3 years kind of wait

e. Autonomous Driving:

4) Value Migration Curve -> Can’t say

a. Not sure, given the company isn’t much active in B2C domain and also current not exploring the ad-markets route to expand revenues.

b. Future strategy pillars mentioned by the company also doesn’t mentions anything on moving up the value chain

c. Drones capabilities & solutions is one on the anvil where they can move up higher in the value chain as the sector is just opening up, but nothing concrete to build a conviction

5) Quality of earnings -> Medium

a. Lumpy sales -> While the auto sales are per-device per year kind of contract, the company also earn revenues by doing implementation works which are bulky in nature

b. Pricing power -> The company has been able to maintain 35-40% PAT margins and contribution margin was going up (except last two quarters where device sales has been pulling down the profits)

6) Key growth drivers

a. Expected Auto 4W and 2W up-cycle -> High

b. Govt regulations and standards which may slowly put a GPS tracker on old as well as new vehicles -> High

c. International Expansion through Mappls-> Uncertain

i. Currently creating digital maps for neighbouring countries of India, but would be lagging behind local players (if any?) as local know-how takes time

ii. The APAC market uptick

d. Waterways? -> Uncertain

7) Intellectual Property – High

The company has been able to develop and launch Mappls which provides Google Maps equivalent on a far lesser budget has been made possible by the company’s in-house IPs and tech team

8) Profitability Drivers

As the company is engaged in leveraging its maps data for delivering solutions to clients, employee expenses, maps updation and advertisements becomes critical to drive the

overall profitability.

a. Employees - Med

The growth in the employee costs (CAGR 4%) is lower than the revenues, therefore reflecting that the company can scale revenues while employee costs may rise at a lower pace.

Additionally the company has lower attrition 12%, 13.5% and 17.5% in FY 20,21,22 respectively

b. Operating Leverage - High

With an operating leverage of 1.5 (in FY 22) reflects that the company has been able to realize higher incremental profitability vs the increase in revenue which is expected from the business model of the company. The higher operating leverage reflects that the company can generate high amount of cash if the revenues grow at a fast pace.

Operating Leverage led by 🗹 Gross Margin 🗹 Asset Turns ◻Product Mix 🗹 Employee Costs

a. Gross Margin

Company has been increasing its Gross Margins consistently, however 9M FY23 has seen a dip due to increase in device revenue which comes at a lower margin

b. Asset Turns

FA Turns has been consistently increasing

c. Product Mix (NA)

As per the management, the margins for either of the lines of business are similar, therefore product mix is not a big contributor for the operating leverage.

c. Employee Cost

The employee costs grow at a slower pace than sales (refer section a above)

KEY MONITORABLE

a) Order Book -> The company’s order book number are disclosed on an annual basis, and typically points towards the revenue that the company is expected to realize over 3-5 years period. Current order book FY 22 ~ 700 Cr.

b) Global expansion -> The company has hired a CEO (20 years experience) for their global business, focusing on the APAC market, cracking of the international markets can be a big trigger for the company.

c) Device Scale-up and subsequent subscription -> While currently the margins of the overall business got muted due to device sales, the management expects subscription revenue to accrued which would come at similar to map-led business i.e. of 53%. The subscription conversions and scale of device sales thus becomes a key monitorable.

Sources referred:

1) Balance sheet and Financial schedules of the company for breakup of expenses

2) Management Discussion and Analysis

3) Annual Report and Investor Presentation, Transcripts and DRHP